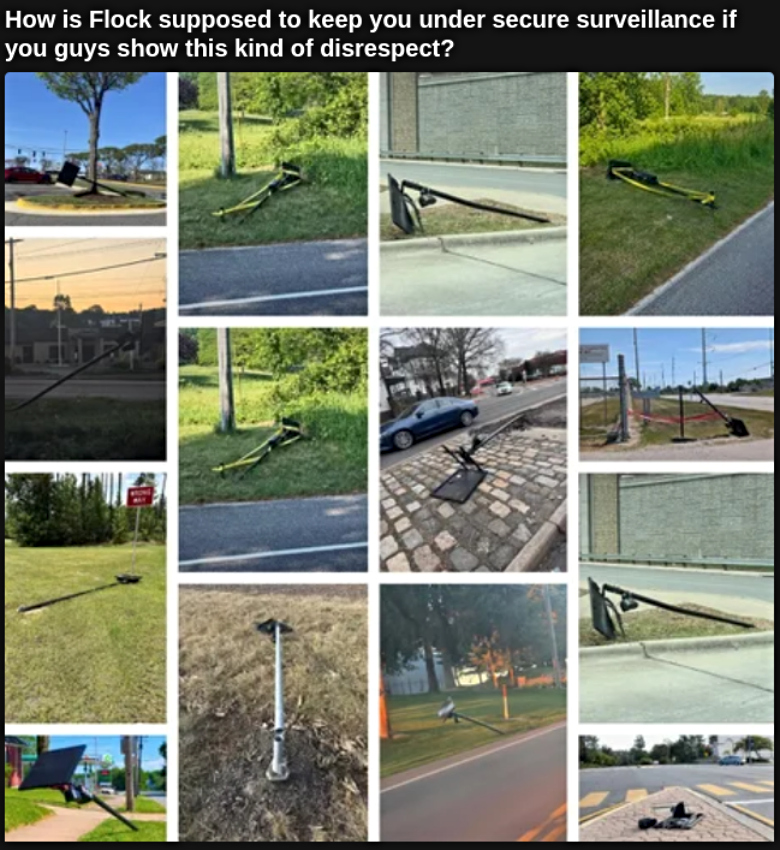

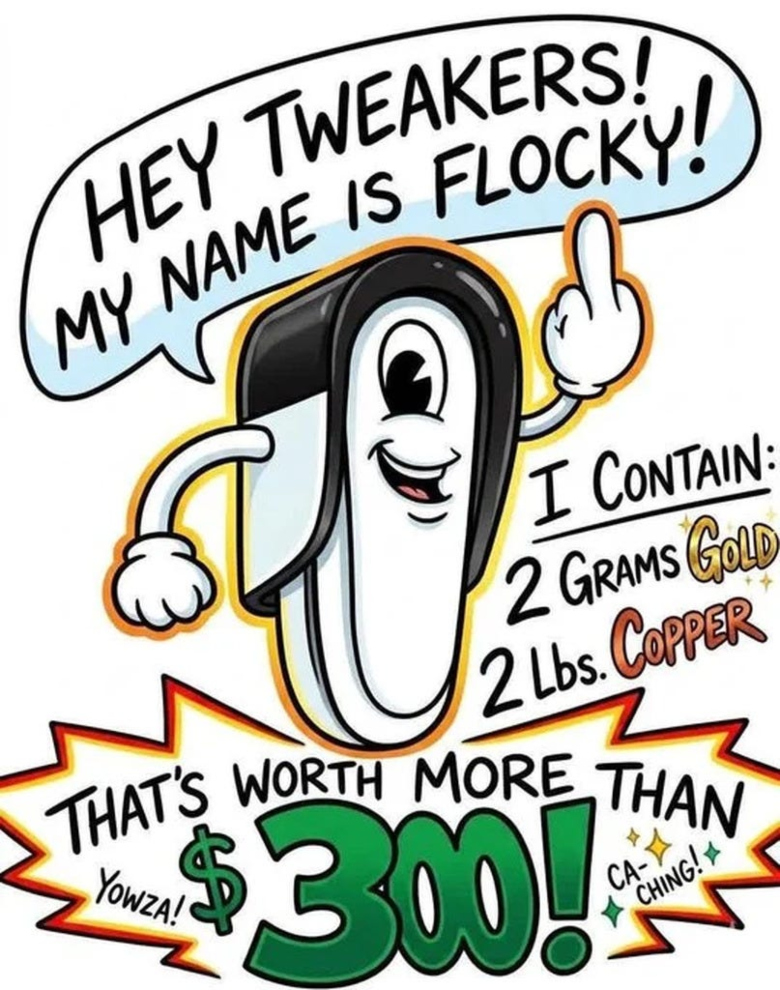

Flock Off: A Collection Of Memes.

Join the Flock resistance: DeFlock.org

Disrupting The Status Quo

Join the Flock resistance: DeFlock.org

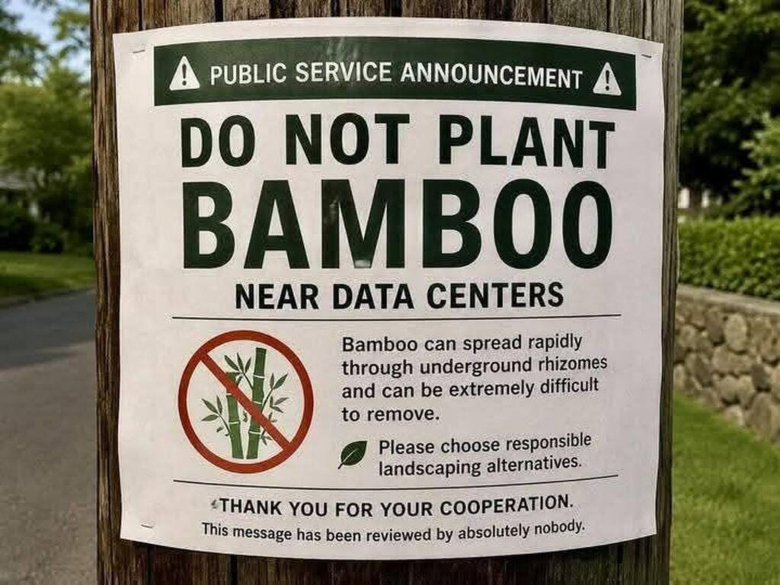

"What we do with an ol' bamboo makes everybody cheer!" - Dick Van Dyke, Chitty Chitty Bang Bang

If you'd like to buy bamboo plants that should never be planted near data centers, here are a few online suppliers:

Plus you can often find it at local garden centers or even find it at Lowes Home Improvement and Home Depot.

If you already have some bamboo, you can divide it and transplant some to a new location:

How to Divide and Transplant Bamboo

You should also probably not plant bamboo where it could grow and block Flock cameras and government-owned surveillance devices. That would be wrong, wouldn't it?

It would also be wrong to plant Kudzu or Giant Hogweed. You definitely don't want to do that. Kudzu is infamous for its rapid growth and ability to smother everything in its path. It can grow a foot a day, covering trees, power lines, and buildings. Giant Hogweed is not only invasive but also poses a health hazard. Its sap can cause severe skin burns. Removal requires protective clothing and careful handling. Who knew gardening could be dangerous?

"When the world wearies and society fails to satisfy, there is always the garden." -- Minnie Aumonier

Governments around the world are working to kill privacy in all its forms, and most people have no idea that it's happening. Even those who know about it don't seem to comprehend how fast it's coming, or how radically it will change their day to day lives. Even fewer have any sort of plan for how to exist in a world where anything they say or do could be recorded and stored for eternity in a giant A.I. powered data center, and can be retrieved at will by any bureaucrat looking to assert his authority or law enforcement officer looking for someone to feed into the court system. Words you typed into social media ten years ago could be found by a system of artificial intelligence that is always looking, always cataloging, and always reporting, making you a prime candidate to send to the for-profit prison system. Thought crimes will become hate crimes in a system that demands obedience and passivity above all else.

Already, cities are filling up with surveillance cameras that stare at us constantly, scanning our faces and recording our license plate numbers. Even a visit to a friend's house results in our images being uploaded by a doorbell camera to a data center, and often these cameras are accessible by law enforcement officials without a warrant. Actually these doorbell cameras don't even need you to approach a house; they can record you casually walking by on a public sidewalk with your wife. Or was that the person you're having an affair with? The camera captures it, either way.

Police forces are now using drones to spy on you from the sky. These drones can hover almost silently hundreds of feet above, videotaping your actions. Want to smoke a joint in your backyard? Look up.

But these aren't the only threats to privacy. Cars will soon be equipped with kill switches so that the police, and possibly others, can shut it off and stop you in your tracks. In-car cameras, already standard in some cars, will silently watch you as you drive. Where is the video sent? Who can view it? Can you have the videos deleted, or are they stored forever, able to be retrieved by strangers with an agenda? The cameras are another layer of surveillance on top of the GPS system built in to most cars now that relay your driving data to a number of third parties, possibly including your insurance company. Even if you don't have GPS, you most likely carry your phone with you everywhere. Today's phones are less communication devices and more surveillance and tracking devices, monitoring everything and selling your data to the highest bidder.

I suppose you could stay home but if you have a "smart" TV, it probably has a camera hidden in the screen plus the ability to record conversations in your home. Any device with voice control, such as Amazon Alexa and some streaming video boxes, could potentially eavesdrop on your most intimate or angry moments. We're told these devices don't watch or listen without our permission, but companies have already been caught violating that promise.

As if all of the above wasn't bad enough, the worst is yet to come. There is a worldwide agenda to lock down the internet. The internet has become the public square, the place where mankind exposes government tyranny and corporate corruption. In a world that is transitioning into a global police state, free and open communication is seen as a threat. At first, social media and "adult" sites (the definition of "adult" sites being extremely vague) are being targeted by requiring users to prove they're legal adults before being able to log in. The verification system used will vary from state to state, but most favor a scheme where your driver's license is uploaded to a third-party company chosen by the government that will confirm you are who you say you are and then provide you with a code to use when accessing restricted sites. Another proposal is more extreme, requiring your computer's operating system to lock you out of restricted sites until your computer receives a code from the third party authorization company. Age verification exposes your true identity to people who don't have to expose their identity to you, and this in turn makes you vulnerable to government officials who want to end free speech and prosecute people for "wrong-think". And once any sort of age verification system is put into place, it will be expanded as part of a full digital ID system that will be used to identify you all day, every day, on the internet and in the real world. Instead of being an independent, free, private person, you'll become a trackable commodity, and the data generated by your mundane living will be sorted and sold and have more value to information brokers than anything you produce in your 9-5 job. But you won't receive any of that value. You're the cow, not the rancher.

And I predict that eventually, within 5 years, all access to the internet will be shut off at the ISP level unless you have permission from the government, which will monitor every keystroke, every site visited, and every comment made, everything dumped into an A.I. data center for review. Speak out against the establishment? Maybe you'll just be "re-educated". Maybe you'll be jailed. Or maybe they'll turn off your bank account for a month or two.

All of these things are either coming soon, or they're already here. So I ask again: Do you have a plan?

Will you quietly obey, try to "go along to get along" in the hope you'll be left alone? Will you risk everything and fight back against this digital tyranny? Will you look for workarounds, such as ways to spoof age verification or avoid ISP blocking? Or will you turn away from the internet and enjoy an analog life, focusing on what's real and can't be shut off from afar?

My own plan is to fight back for as long as I can and hope someone smarter than me invents a private, functional way around the tyranny. If that way doesn't appear, I'll stop using all internet-connected devices except when absolutely necessary to survive, such as buying food, renewing my driver's license, or paying a bill. As for all the cameras and drones, the defensive options are very limited. Moving to a rural area and limiting time spent in cities and on highways is about all we can do at this point until better solutions are found.

For now, I'm buying a lot of books, real books, printed on paper, that can never be censored once they're on my shelf.

Because the digital world is a trap. The future is analog.

[Image by Riki32 from Pixabay]

Related Articles:

Federal Surveillance Tech Becomes Mandatory in New Cars by 2027

AI Spy Cameras Suddenly Blanketing America

The FBI Wants The Ability To Surveil Americans With Biometric AI Drones

Illinois House Bill Would Force Operating Systems To Check Your Age

Massachusetts House Passes Social Media Age Verification Digital ID Bill

US Bill Mandates On-Device Age Verification

Trump’s Palantir-Powered Surveillance Is Turning America Into A Digital Prison

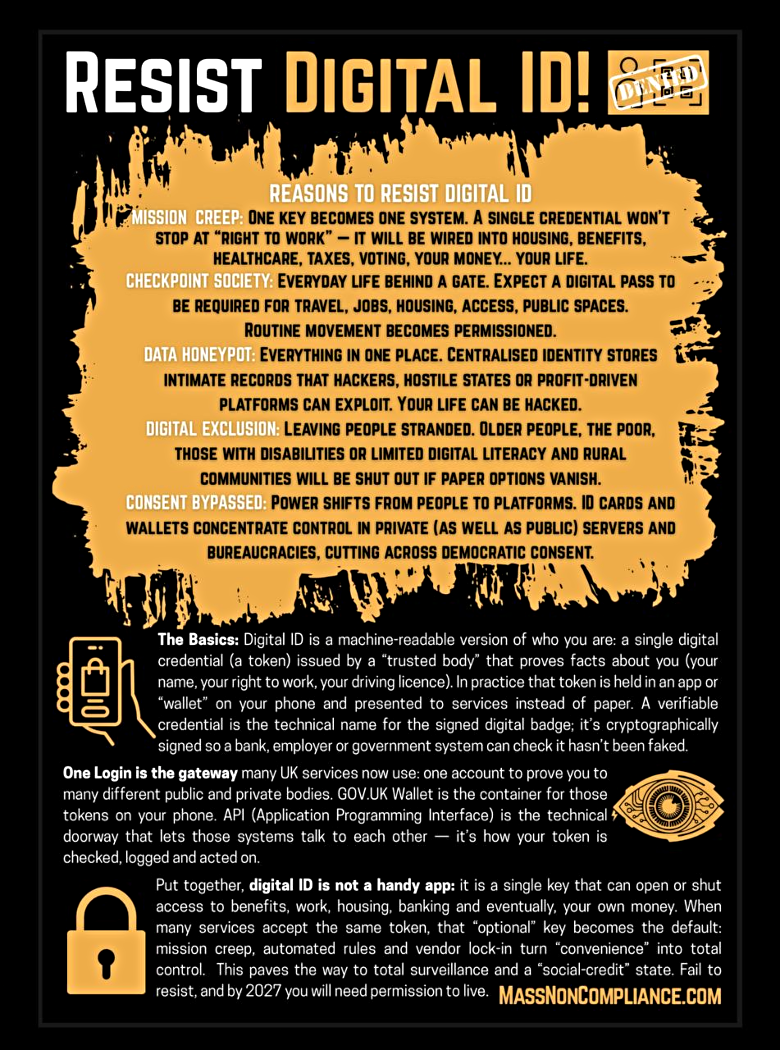

"We are at the brink. Fear and propaganda are the sales pitch. Digital ID is the product. It is marketed as safety but built for control. If you accept digital ID now, it may be the last real choice you ever make."

Despite the lies being told to us by politicians, technocrats, and news media propagandists, digital ID isn't being introduced to protect us, or to make life more convenient, or to stop illegal immigration. Digital ID is nothing but a tool of control by the world's wealthiest people who want to own everything on the planet...and that includes every one of us who can't afford to buy our own freedom. Digital ID is a step toward a global feudal economy, the introduction of slavery on a scale the world has never seen before, enforced by artificial intelligence, drones, robots, and any corrupt police officers willing to sell out humanity for a steady paycheck.

Do you really think they're building all those massive data centers to make your internet searches easier? No, those centers are being built so our lives can be tracked and controlled from cradle to grave -- everything we do, everything we buy, every place we go, everyone we interact with, and one day, all of our thoughts -- cataloged and analyzed by amoral machines that will decide what is best for us. Freedom, gone. Creativity, gone. Love and joy, gone.

We're closer to this dystopian future than most people realize. And it starts with digital ID, if we allow it.

A group of people in the United Kingdom are on the front lines taking action to inform the public about the dangers of digital ID and also giving advice on how to resist its implementation. I've republished one of their action plans above but there's more available on their website, massnoncompliance.com. Although the site is focused on the UK, don't be complacent. Digital ID is being rolled out worldwide, including in the United States. The "Real ID" scheme in the U.S. is the first phase of its introduction here.

I urge you to learn more about digital ID and then do your part to stop it.

The alternative is, quite frankly, slavery.

[for a pdf download of the action plan above, click here]

"Imagine a future where access to work, healthcare, or travel can be cut off simply by flipping a digital switch. This slow normalization of digital ID is the frog in a boiling pot: Each step seems harmless until the system is fully established and resistance becomes nearly impossible." -- Elizabeth Lawrence

I don’t know whether or not the trolls, the shills, the 77th brigade and the rest of the detritus who sneered and whinged and helped the covid 19 hoax promoters destroy the lives of many millions are already stalking the peaceful halls of Substack. But if they’re not here yet they soon will be as we enter the next stage of our enforced journey through the Gates of hell and into the great reset and the new world order. I shan’t see them and I advise you to ignore them. They thrive on attention. Let them scream silently into the dark of the wilderness they have created for themselves.

They will moan and lie and deceive and threaten for their purpose is to confuse and to throw dark shadows into places where light is shone. They will tell us how ID cards will save us and how and why we must abandon our freedom and privacy for their greater cause.

They aim to deceive with their ignorance, their private brands of pseudoscience and their hatred and their allegiance to the Bilderbergers, the WEF, the UN, the globalists, the global warming freaks, the pro vaxxers and the rest of them.

The battle now is against the ID cards which will lead us to a digital world, a cashless society, the evils of social credit, vaccine passports and the deliberate exclusion from society of those who care for humanity, for peace, for caring, for respect, honour and dignity.

This was always going to be our last stand.

We will, make no mistake, be fighting for our lives and for the future of mankind.

We must stay strong, link arms and stand together in the light.

Dr. Vernon Coleman

================

To see more of Dr Coleman's work, please visit his Substack page.

Image by Pete Linforth from Pixabay.